Lecture

In this  we prove one of the simplest, but at the same time the most important forms of the law of large numbers - the Chebyshev theorem. This theorem establishes a connection between the arithmetic mean of the observed values of a random variable and its expectation.

we prove one of the simplest, but at the same time the most important forms of the law of large numbers - the Chebyshev theorem. This theorem establishes a connection between the arithmetic mean of the observed values of a random variable and its expectation.

First we solve the following auxiliary problem.

There is a random variable  with mathematical expectation

with mathematical expectation  and variance

and variance  . Above this value is

. Above this value is  independent experiments and calculates the arithmetic average of all observed values of . It is required to find the numerical characteristics of this arithmetic average - the expectation and variance - and find out how they change with increasing .

independent experiments and calculates the arithmetic average of all observed values of . It is required to find the numerical characteristics of this arithmetic average - the expectation and variance - and find out how they change with increasing .

Denote:

- value in the first experience;

- value in the first experience;

- value in the second experiment, etc.

- value in the second experiment, etc.

Obviously, a set of values  represents independent random variables, each of which is distributed according to the same law as the quantity itself . Consider the arithmetic average of these values:

represents independent random variables, each of which is distributed according to the same law as the quantity itself . Consider the arithmetic average of these values:

.

.

Random value  there is a linear function of independent random variables . Find the expectation and variance of this value. According to the rules 10 to determine the numerical characteristics of linear functions, we obtain:

there is a linear function of independent random variables . Find the expectation and variance of this value. According to the rules 10 to determine the numerical characteristics of linear functions, we obtain:

;

;

.

.

So, the expected value of does not depend on the number of experiences and equal to the expected value of the observed value ; as for the variance of magnitude then it decreases unlimitedly with an increase in the number of experiments and with a sufficiently large can be made arbitrarily small. We see that the arithmetic mean is a random variable with an arbitrarily small variance and, with a large number of experiments, behaves almost as not random.

Chebyshev's theorem establishes in exact quantitative form this property of stability of the arithmetic mean. It is formulated as follows:

With a sufficiently large number of independent experiments, the arithmetic mean of the observed values of a random variable converges in probability to its expected value.

We write the Chebyshev theorem as a formula. For this we recall the meaning of the term "converges in probability." It is said that a random variable  converges in probability to value

converges in probability to value  if increasing probability that and will be arbitrarily close, unlimitedly approaching unity, which means that with a sufficiently large

if increasing probability that and will be arbitrarily close, unlimitedly approaching unity, which means that with a sufficiently large

,

,

Where  - arbitrarily small positive numbers.

- arbitrarily small positive numbers.

We write in a similar form the Chebyshev theorem. She claims that while increasing average  converges in probability to i.e.

converges in probability to i.e.

. (13.3.1)

. (13.3.1)

Let us prove this inequality.

Evidence. Above it was shown that

has numeric characteristics

;

;  .

.

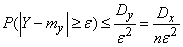

Apply to random value Chebyshev's inequality, believing  :

:

.

.

No matter how small the number  you can take so big that inequality holds

you can take so big that inequality holds

Where  - arbitrarily small number.

- arbitrarily small number.

Then

,

,

whence, moving to the opposite event, we have:

,

,

Q.E.D.

Comments

To leave a comment

Probability theory. Mathematical Statistics and Stochastic Analysis

Terms: Probability theory. Mathematical Statistics and Stochastic Analysis